Top 3 retirement planning benefits offered by annuities

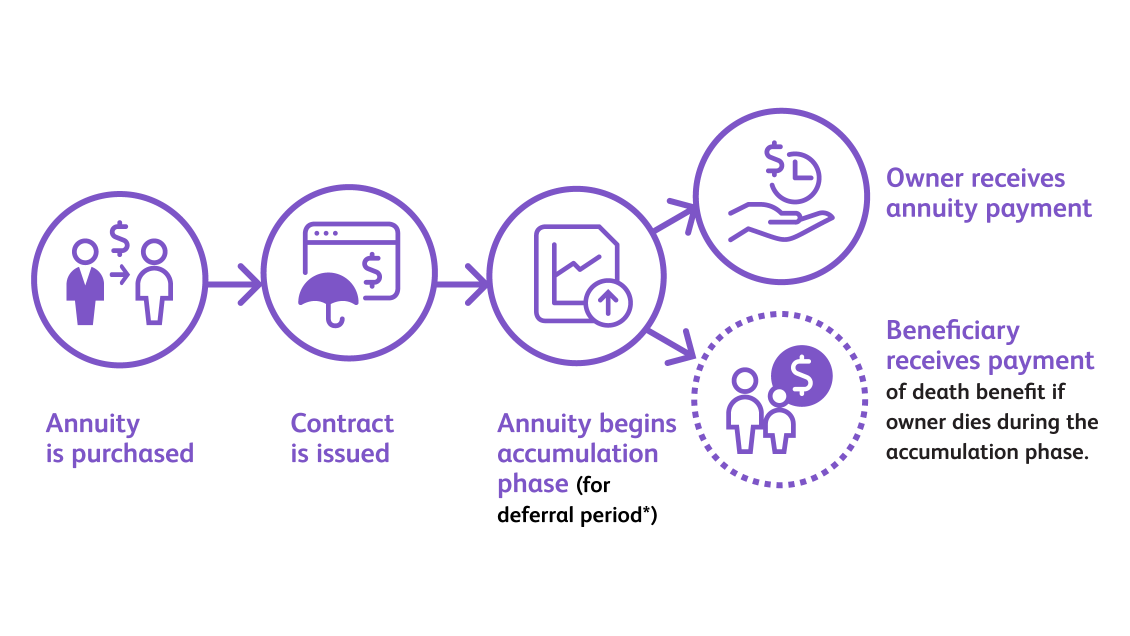

Explaining the 2 phases of annuities

Basic annuity designs: immediate or deferred?

Explore the different types of annuities

Compare features for the ideal fit

Other related topics

*An immediate annuity will not have an accumulation phase

Annuities are long-term insurance contracts intended for retirement planning. Annuities also may be subject to income tax and, if taken prior to age 59 ½, an additional 10% IRS tax penalty may apply. Because Protective and its representatives do not offer legal or tax advice, it is important that you talk with your own legal and tax advisor about your specific tax situation.

Investors should carefully consider the investment objectives, risks, charges and expenses of a variable annuity and the underlying investment options before investing. This and other information is contained in the prospectuses for a variable annuity and its underlying investment options. Prospectuses may be obtained by contacting PLICO at 800-265-1545.

An indexed annuity is not an investment in an index, is not a security or stock market investment and does not participate in any stock or equity investments.

WEB.3147009.09.21